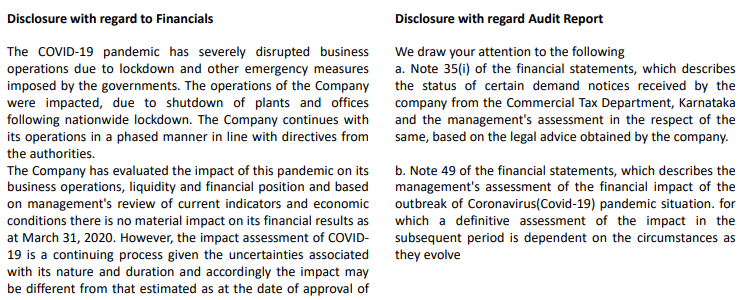

All listed entities are required to disclose the impact of #Covid-19 on their financial statements in their results. Detailed disclosures are also required in notes. The auditor is also required to comment on the same in his audit report. In the attached file, we have compiled disclosures made by various companies in this regard. Hope you will find it useful.

Read More: https://adobe.ly/2XNViup

One, better travel and accem- modation facilities. In case of large assignments, travel and accommodation is an integral part of the assignment. Staff put up near the client office in hotels or guest houses can lend better time to work than those residing far away. Cities are crowded and commuting can be a painful experi- ence. In fact, it is common today to see instances where even the audit staff residing in the same city are put up in a hotel near the client office to save time in daily commute. For this reason, large assignments may not be disadvantaged by the absence of a local office.

One, better travel and accem- modation facilities. In case of large assignments, travel and accommodation is an integral part of the assignment. Staff put up near the client office in hotels or guest houses can lend better time to work than those residing far away. Cities are crowded and commuting can be a painful experi- ence. In fact, it is common today to see instances where even the audit staff residing in the same city are put up in a hotel near the client office to save time in daily commute. For this reason, large assignments may not be disadvantaged by the absence of a local office.